Running a nonprofit is like planting a tree, but what if the soil (your funding) keeps drying up? Financial sustainability is when your nonprofit has sufficient money the help people and there is no loss of money. I’m here to share what financial sustainability is, why it’s critical, and how you can build it for your nonprofit. Let’s look at easy, real-world steps to help your organization last and do well for many years.

Financial sustainability means your nonprofit has enough money to run programs and pay bills consistently. It mixes income sources, spends wisely, and saves for surprises.

Quick Snapshot

Easy ways to make donors love supporting you.

- What financial sustainability means for your nonprofit.

- 10 easy ways to keep your money steady.

- Mistakes to avoid that could hurt your budget.

- How to plan for a financially healthy future.

- Questions to boost your nonprofit’s money plan.

Wondering how to keep your nonprofit’s funds safe? I’ll answer these.

Table of Contents

What happens if your nonprofit runs out of money?

If your nonprofit runs out of money, programs stop, staff may leave, and your mission suffers. Mix income sources and save 3–6 months of expenses to avoid financial troubles and keep helping people.

Running out of money can halt your nonprofit’s programs. You might lose staff or cut services, hurting your mission. I’ve seen groups avoid this by mixing income and saving. Start building a safety net to keep your nonprofit strong.

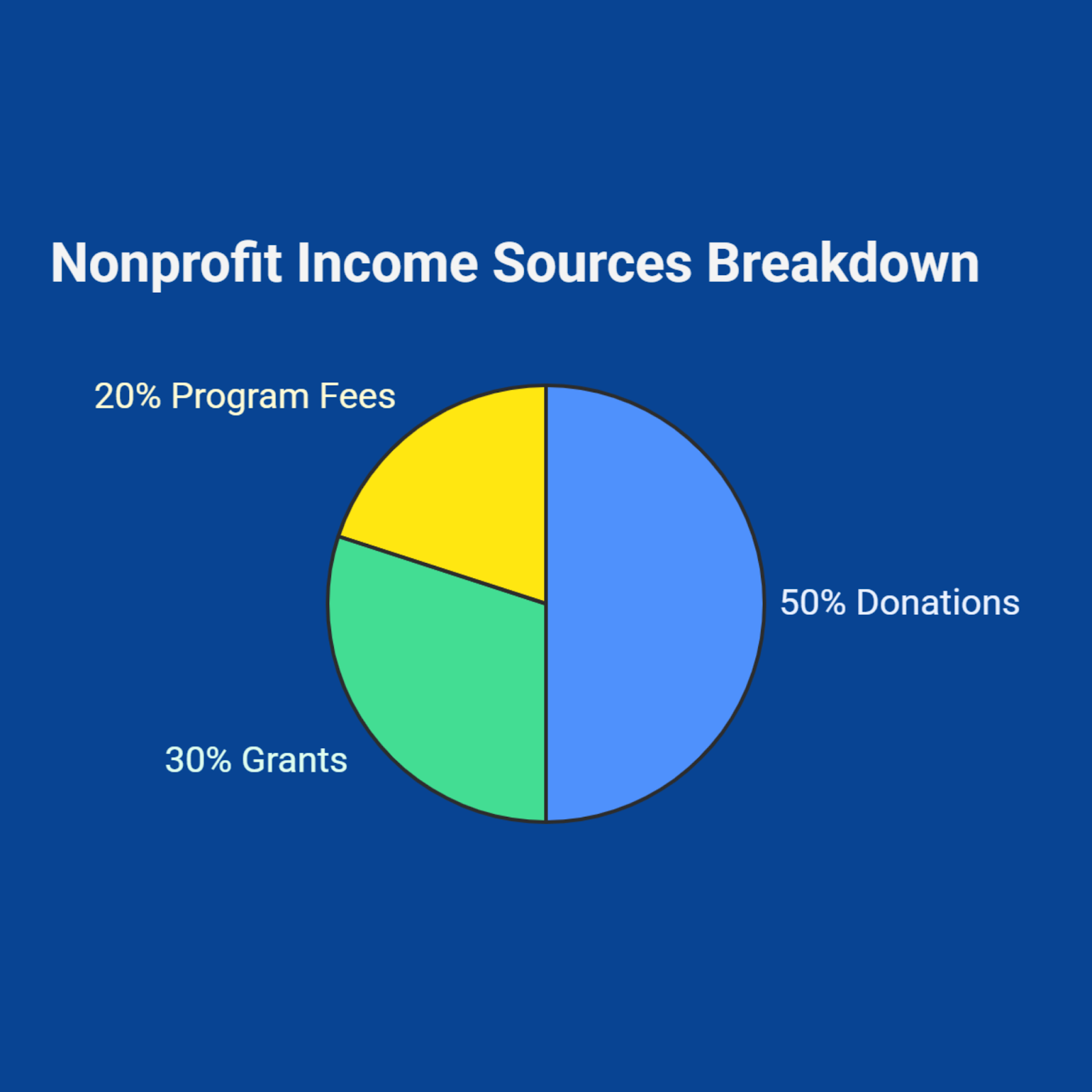

How can you bring in money from different places?

Bring in money from donations, grants, event tickets, memberships, workshop fees, and crowdfunding. Mixing these sources creates a safety net, so you’re not stuck if one fund stops.

You can raise funds from donations, grants, and event tickets. Add memberships or workshop fees for steady cash. Crowdfunding online reaches new donors. Mixing these keeps your nonprofit safe if one source dries up.

What steps can you take to avoid money troubles?

Don’t rely on one fund, like a single grant; it’s risky. Save 3–6 months of expenses for emergencies. Track every penny to avoid small costs adding up. Good Nonprofit Financial Management means using tools like QuickBooks to stay organized and keep your budget strong.

What is Financial Sustainability for Nonprofits?

It’s when your nonprofit has steady funds to run smoothly over time. You mix income, spend smart, and save for surprises to focus on your mission.

Picture your nonprofit as a sturdy house. Financial sustainability is the strong base that keeps it standing. It means you have enough cash to cover programs, staff, and unexpected costs without worry.

You might get donations or grants. Relying on just one is risky. Sustainability mixes incomes, like event tickets or memberships. This helps you focus on helping people, not just paying bills.

Why is Financial Sustainability Important?

Sustainability keeps your nonprofit running, builds donor trust, and helps you plan ahead. It stops money worries so you can focus on your mission.

Ever wonder why some nonprofits grow while others struggle? A solid money plan makes the difference. Here’s why it matters:

- Focus on Your Mission: Regular money means you can help people without stress.

- Donor Trust: People give more when they see you handle money well. It shows you’re reliable.

- Plan for Growth: Extra cash saved helps you start new programs without fear.

Without a strong plan, one lost grant could shake your nonprofit. Keeping cash steady helps nonprofits succeed. You can get there too!

10 Strategies to Build Financial Sustainability

Here are 10 simple ways to make your nonprofit’s finances strong. I’ve added examples and two tables to show how they work:

1. Mix Up Your Income

Counting on one funder is like eating only one food. You need variety! I know a community group that added class fees and small donations to their grants. They stayed strong when one fund ran low. Here’s a table of income ideas:

| Income Type | What It Is | How to Start | Why It Helps |

| Donations | Gifts from supporters | Ask for small, regular gifts | Brings steady cash |

| Grants | Money from foundations | Apply to funders who match your mission | Funds big projects |

| Event Tickets | Fees for events, like galas | Host a fun fundraiser | Adds extra money |

| Memberships | Annual fees from members | Offer benefits, like updates | Creates loyal supporters |

| Workshop Fees | Charges for classes or training | Teach your skills to locals | Turns expertise into cash |

| Crowdfunding | Online campaigns for small gifts | Start a quick online drive | Reaches new donors |

Source: Original data based on nonprofit best practices.

Mixing up your income sources builds a safety net, keeping your nonprofit strong no matter what funding surprises pop up.

With diverse income in place, let’s talk about saving for those rainy days.

2. Save for Emergencies

A savings fund is like a life jacket for your nonprofit. I saw a tutoring program save a little each month. They easily paid for a surprise cost, like a broken computer. With the right planning, or support from a Fractional CFO, you can aim for 3 to 6 months of bills.

- Put away 5% of extra money each month.

- Use unexpected gifts, like event profits, to save.

An emergency fund is like a life preserver, ready to keep your nonprofit afloat during tough times.

Now that you’ve got a savings plan, let’s explore how to lock in steady cash.

3. Get Monthly Donors

Monthly donors are like loyal friends. They keep giving. A pet shelter I helped got $15 monthly pledges that added up fast. Make sign-up easy and show how gifts help.

- Offer small amounts, like $10 or $20 a month.

- Share stories, like how $10 feeds a kitten.

Monthly giving turns small donations into a reliable stream, fueling your mission without stress.

Steady donors are awesome, but let’s see how your skills can bring in extra funds.

4. Earn Money with Your Skills

Your nonprofit’s talents can make cash. A literacy group I know sold reading classes to schools. Find what you’re great at and charge for it.

- Offer workshops, consulting, or mission-related items.

- Check what others charge to set fair prices.

Your nonprofit’s know-how is a goldmine that can spark new income to power your programs.

With new revenue flowing, let’s focus on keeping your donors coming back.

5. Keep Donors Happy

Keeping donors is easier than finding new ones. A food bank I saw sent thank-you notes and updates. Donors felt special and kept giving. Here’s a table of ways to keep donors:

| Action | What It Does | How Often | Why It Works |

| Thank-You Note | Shows gratitude for gifts | Within 2 days | Makes donors feel valued |

| Impact Update | Shares how their money helped | Monthly | Keeps donors excited |

| Program News | Updates on your work | Every 3 months | Builds trust and connection |

| Personal Call | Direct thank-you from staff | Yearly for big donors | Creates strong loyalty |

| Event Invite | Invites donors to events | Yearly | Makes them feel part of the team |

| Annual Report | Shows all your achievements | Yearly | Proves their gift made a difference |

Source: Original data based on nonprofit donor practices.

A solid donor stewardship plan turns one-time givers into loyal friends for your nonprofit’s journey. Loyal donors are key, so let’s build smart systems, like strong tracking and Charity Bookkeeping Solutions, to make your finances shine.

6. Use Simple Financial Tools

Good tools make managing money easy. A health group I worked with used software to track funds. It saved hours. Tools like QuickBooks help, as noted by Nonprofit Accounting Basics.

- Try accounting software or donor tracking apps.

- Check your budget each month to stay on track.

Smart financial tools streamline your work, making growth smooth and stress-free.

With systems sorted, let’s dive into winning grants to boost your budget.

7. Write Great Grants

Grants can bring big money. You need a plan. I saw an arts group win funds by picking funders who loved their work. Research well and follow their rules.

- Find funders who match your mission.

- Send clear applications early.

Smart grant writing opens doors to big funds, giving your nonprofit a financial edge.

Grants are great, but let’s see how tech can take your fundraising strategy to the next level.

8. Use Technology to Raise Funds

Tech makes fundraising fun and fast. A women’s shelter I know used email campaigns to get more donations. It’s like a helper that works all day, per Donorbox.

- Send automatic emails asking for gifts.

- Check which messages get the most clicks.

Using tech wisely can ramp up your fundraising, bringing in more cash with less effort.

With tech boosting your funds, let’s get your board to join the fundraising party.

9. Get Your Board to Help

Your board can raise money if you guide them. A community center’s board hosted fun events. They brought in extra cash. Give them easy ways to help.

- Set goals, like each member raising $500.

- Train them with simple scripts or ideas.

An active board can work magic, raising funds to lift your nonprofit’s mission higher.

Your board’s ready to roll, so let’s wrap up with planning for the long haul.

10. Plan for the Future

A long-term plan is your nonprofit’s map. I helped a nature group make a 3-year plan to grow their budget. Think big but start small to keep your mission strong.

- Set goals, like doubling your savings.

- Check your plan each year to stay on track.

| Planning Step | What It Does | How to Do It | Why It Helps |

| Set Financial Goals | Defines your budget targets | Aim to double savings or add a program | Gives clear direction |

| Check Budget Yearly | Tracks spending and income | Review expenses each year | Keeps you on track |

| Plan New Programs | Expands your mission | Budget for one new project | Grows your impact |

| Build Reserve Fund | Saves for emergencies | Save 5% of income monthly | Protects against surprises |

| Engage Board | Gets board to plan | Hold yearly strategy meetings | Strengthens leadership |

| Monitor Fundraising | Tracks donation trends | Check donor data quarterly | Boosts steady income |

Source: Original data based on nonprofit planning practices, inspired by nonprofit budgeting guide.

A long-term plan is like a map. It keeps your mission on track year after year.

Mistakes to Avoid

Don’t let these errors hurt your nonprofit:

- Sticking to One Fund: If one grant pays most of your bills, you’re in trouble if it ends. Mix your income to stay safe.

- Ignoring Small Costs: Things like extra pens or snacks add up. Watch every penny.

- Skipping Savings: Without savings, one problem could stop your work. Start saving now, even a little.

Plan for Long-Term Success

To keep your nonprofit strong, make a 3-to-5-year plan. Set goals, like growing your savings or starting a new program. I’ve seen groups stay steady by checking their plan each year. Need help? Fincera Accounting can guide you.

Think about these to boost your nonprofit’s finances.

Are you relying too much on one money source?

Relying on one fund, like a grant, risks your nonprofit if it stops. Mix income from donations, events, and fees to stay stable and keep your mission going.

Depending on one fund, like a single grant, is risky. If it stops, your nonprofit could struggle. Mix income from donations, event tickets, and memberships. This keeps your budget steady and safe.

Do you have savings for tough times?

Savings for 3–6 months of bills protect your nonprofit from surprises, like broken equipment. Start small, like $50 a month, to build a strong emergency fund.

You need savings to handle surprises, like a broken computer. Aim for 3-6 months of expenses. Start small, saving $50 a month. It’s like a safety net for your nonprofit’s mission.

How can you make donors feel special to keep giving?

Send thank-you notes within days to show gratitude. Share monthly updates on how gifts help. Invite donors to events to build connections. These steps make donors feel valued and keep them giving.

Summary

Here’s what you’ve learned:

- Financial sustainability keeps your nonprofit’s mission alive with steady funds.

- 10 strategies, like mixing income and saving, build a strong budget.

- Avoid mistakes, such as relying on one fund, to stay safe.

- Plan for the future to make your nonprofit grow and last.

The Bottom Line

Financial sustainability for nonprofit organizations is more than just balancing your budget. It’s about making sure your nonprofit can keep helping people without money worries. I’ve seen steady funds let groups expand programs and earn donor trust. It’s your key to a lasting mission and fearless growth.

Ready to Strengthen Your Nonprofit’s Finances?

Struggling to balance your nonprofit’s budget? Mix your income sources and save a little each month to build financial sustainability for nonprofit organizations. Let’s chat about your goals. Book a free NYC consultation with Fincera today.

FAQs

How do nonprofits stay financially stable?

Financial sustainability for nonprofits comes from mixing income sources like donations, grants, and event fees.Saving 3 to 6 months of money helps you deal with emergencies. I’ve seen groups thrive by using tools like QuickBooks to track every penny. Regular donor updates build trust, keeping funds flowing. Start small, like setting aside $50 a month, and check your budget yearly to stay on track.

What are the biggest financial risks for nonprofits?

Nonprofit financial risks often stem from relying on one funding source, like a single grant. If it stops, your programs could stall. Small, unchecked expenses, like office supplies, can also drain your budget. I’ve worked with groups that lost donors due to poor money management. Mix income, track spending, and save for emergencies to keep your nonprofit safe and focused on its mission.

How can nonprofits attract more donors?

Attracting nonprofit donors starts with sharing clear, emotional stories about your impact. I’ve seen shelters double donations by sending monthly updates showing how gifts help, like feeding a pet. Offer easy giving options, like $10 monthly pledges. Host fun events to connect with supporters. Build trust by showing smart money use, encouraging more people to give to your cause.

Why do nonprofits struggle with money?

Nonprofit funding struggles often happen when groups depend on one big fund, like a grant, which can stop suddenly. I’ve seen nonprofits falter by ignoring small costs that add up, like extra snacks. Skipping savings leaves you vulnerable to surprises, like equipment breakdowns. Mix income from donations and fees, save monthly, and use budgeting tools to keep your nonprofit strong and stress-free.

How much should nonprofits save for emergencies?

Nonprofit emergency savings should cover 3–6 months of operating costs, like rent and salaries. I helped a tutoring program start with $50 monthly savings, growing to $15,000 in a year. This protects against surprises, like a broken computer. Set aside 5% of extra income each month. Check your savings goal yearly to ensure your nonprofit stays secure and focused on its mission.

Can small nonprofits achieve financial sustainability?

Financial sustainability for small nonprofits is absolutely possible with smart planning. I’ve seen tiny groups succeed by mixing income from small donations, local events, and online crowdfunding. Use free tools, like Google Sheets, to track funds. Thank donors quickly to keep them giving. Start saving a little each month and set a 3-year plan to grow your impact without financial stress.

How do you create a nonprofit budget that lasts?

Nonprofit budget stability starts with listing all income sources, like donations and grants, and tracking every expense. I’ve helped groups cut small costs, like unused subscriptions, to save thousands. Plan for 3–6 months of emergency funds. Review your budget yearly to adjust for new programs. Use tools like QuickBooks, as noted in nonprofit accounting basics, to keep your finances clear and sustainable.

What role does transparency play in nonprofit funding?

Nonprofit funding transparency builds donor trust, encouraging more giving. Share clear reports showing how every dollar is spent, like program costs versus overhead. I’ve seen groups gain loyal donors by sending annual impact reports. Be open about financial challenges and how you solve them. This honesty, paired with smart budgeting, proves your nonprofit is reliable, keeping supporters invested in your mission for the long haul.